Nokia Q1 2026: What This Really Means for Telecom Industry

By NextGComm| 24 April 2026

Summary

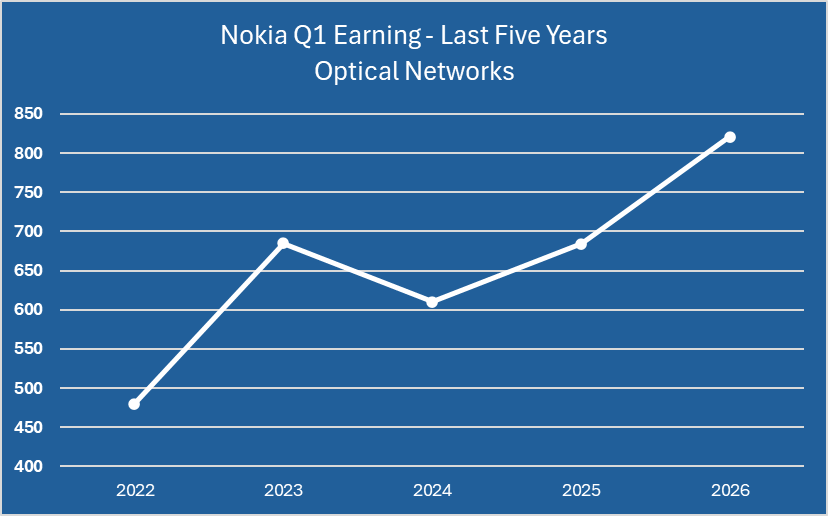

- Optical Networks is exploding: ~20% growth, driven by AI and data center demand

- AI & Cloud is no longer experimental: ~49% growth, now 8% of total revenue

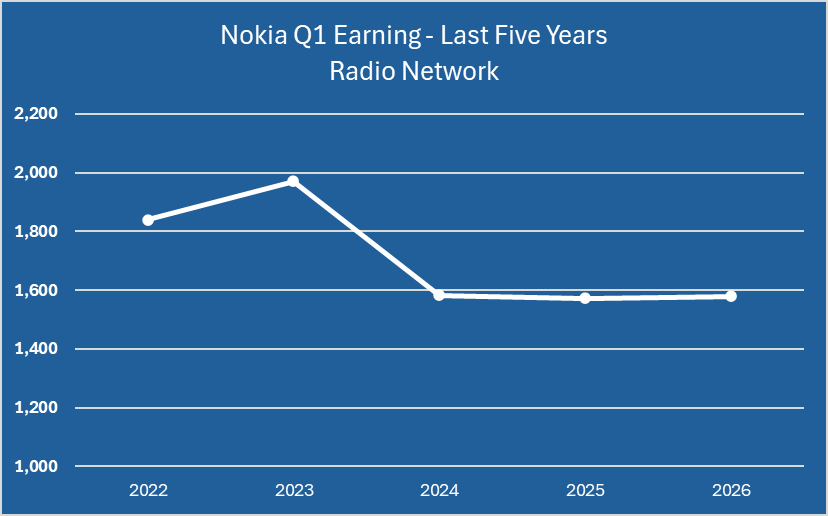

- RAN is flat → classic mobile network cycle still weak

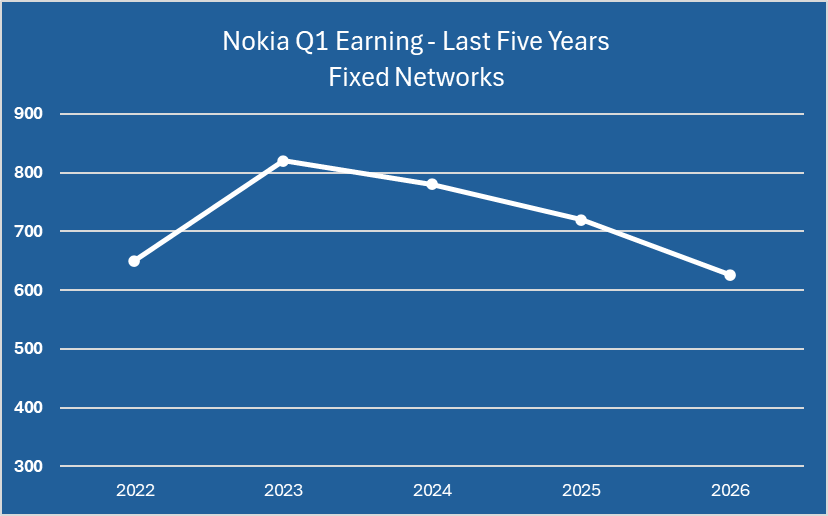

- Fixed Networks declining → legacy access business under pressure

Growth is shifting away from traditional telco toward AI-driven infrastructure

Do you still remember the Nokia tagline" Connecting People". In November 2025, Nokia changed its tagline from "Connecting People" to "Connecting Intelligence". It was a new strategic move by new Nokia CEO Justin Hotard. The company is clearly building a new base around the AI supercycle, not around the 10-year-old telecom replacement cycle. And this Q1 report has clearly shown why it is the right move.

Last year, Nokia acquired optical networking giant Infinera to dominate the optical networks market, positioning itself as the second-biggest revenue generator in this segment with $821 million, and capturing approximately 30% of the global optical market share.

Let's take a quick look on the earning result numbers and trends of Nokia's two main business segments

Network Infrastructure Segment:

Optical networks products demand continues to grow primarily driven by AI & Cloud sector where we see significant order intake growth after winning additional significant opportunities in the quarter.

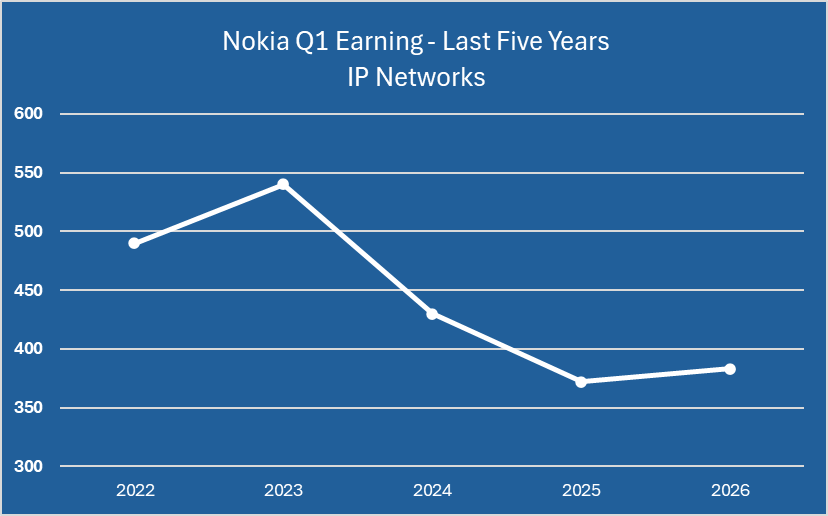

IP Networks net sales increased 3% on a constant currency basis with growth from AI & Cloud, which was partially offset by a decline from Telecommunication Providers.

Fixed Networks net sales declined 13% on a constant currency basis. The decline was primarily due to a decline in sales of consumer premise fiber related products as Nokia focus the business towards higher margin products.

Normally, a double-digit drop in sales is a red flag, but Nokia is framing this as a deliberate strategic choice rather than a loss of market share.

Mobile Infrastructure Segment:

Radio Networks net sales was stable on a constant currency basis. Growth in EMEA and Latin America was offset by a decline in North America related to a prior contract loss from December 2023.

Core Software net sales grew 5% on a constant currency basis.

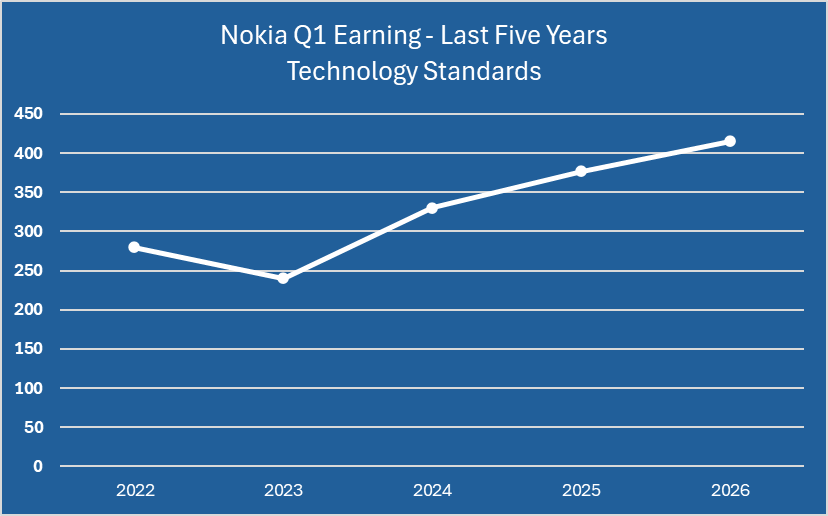

Technology Standards delivered net sales of EUR 385 million in the quarter, growing 10% on a constant currency basis. In the quarter Nokia signed several deals in consumer electronics and multimedia that contributed catch-up net sales to the quarter.

Key Takeaways

Nokia's Q1 results are not a routine earnings beat rather they mark a meaningful inflection in the company's strategic positioning. Several conclusions stand out for leaders tracking the telecom equipment landscape.

The AI supercycle is Nokia's new north star. Over EUR 1 billion in AI & Cloud orders booked in a single quarter signals a structural demand shift, not a cyclical uptick. Nokia is no longer competing primarily on the telecom replacement cycle; it is repositioning itself as infrastructure for the next wave of compute-intensive networking.

Optical Networks is the crown jewel. Twenty percent growth, book-to-bill above one, and accelerating investment in the San Jose indium phosphide facility point to a business with genuine pricing power and supply-demand tension in its favor. This is where Nokia's long-term margin story will be written or lost.

Portfolio discipline is being exercised, Nokia is explicitly shifting away from lower-margin activity in Fixed Networks and has moved non-core units into Portfolio Businesses while it evaluates strategic option. This is a clear signal that strategic focus is real.

RAN remains a managed asset, not a growth engine. Flat constant-currency performance confirms the radio market is competitive and commoditizing. The smart play is defending key accounts and protecting margin, not chasing volume.

Prediction on HR counts impacts:

We predict that Nokia will swing towards targeted hiring during next quarter, not broad hiring. Nokia is increasing investment in Optical Networks, ramping a new manufacturing facility later this year, pushing IP Networks deeper into AI/data-center use cases, and preparing AI-RAN trials later in 2026. Those are all areas that usually require more engineering, manufacturing, supply-chain, field application, validation, and customer-program talent.

At the same time, the report is explicit about cost savings, restructuring charges, and moving non-core assets into a separate portfolio bucket. That means headcount pressure will remain in legacy, low-growth, or non-core areas. So the employment impact is likely bifurcated: more opportunity in optical, IP, AI/cloud, core software, and integration roles; less room for slow-growth support functions and portfolio businesses.

Notably, Nokia's newly appointed Chief People Officer Kristen Pressner recently joined the leadership team, bringing over 30 years of global HR and organizational transformation experience. Her appointment signals Nokia's intent to take a more strategic and deliberate approach to talent and culture while aligning its workforce with the demands of the AI era, rather than simply maintaining the status quo.